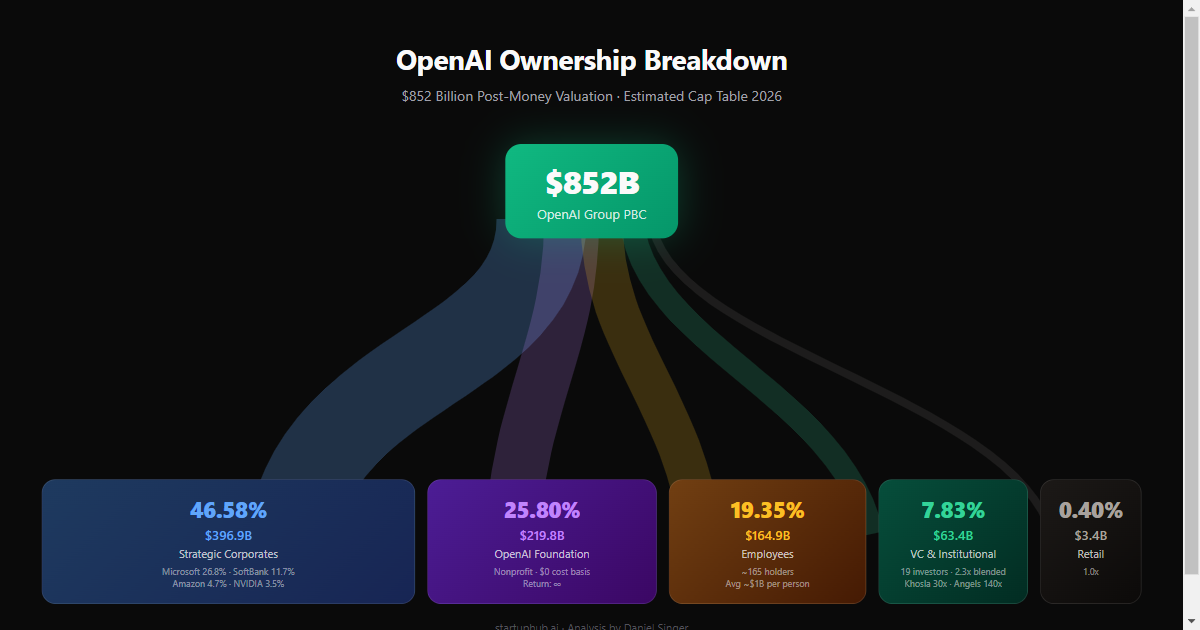

Somewhere on Sand Hill Road this week, a spreadsheet is making the rounds. Twenty-nine lines. Five columns of numbers. It is, by any reasonable measure, the most extraordinary document in the history of venture capital. A reconstructed cap table showing who owns OpenAI at its $852 billion post-money valuation, what they paid, and what their stakes are worth today.

The numbers are staggering. A nonprofit foundation holding $219.8 billion in paper value. A single corporate partner sitting on $215 billion in unrealized gains. Early angel investors, including Reid Hoffman and Peter Thiel, who wrote checks when "artificial general intelligence" was still a punchline, watching their $10 million turn into $1.4 billion. That is a 140x return. It may be the most lucrative angel bet in history.