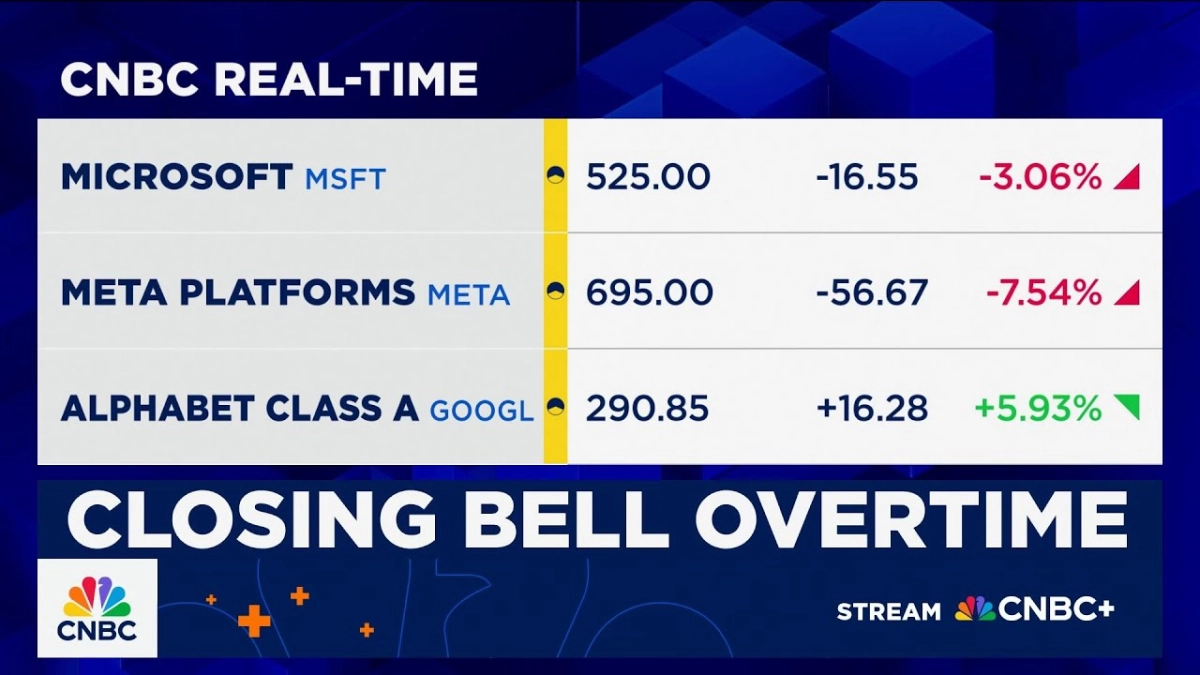

The prevailing market skepticism around AI's immediate profitability finds a powerful counter-narrative in Microsoft's recent earnings, suggesting a robust monetization strategy is already underway. Brent Thill, a Software & Internet Research Analyst at Jefferies, speaking on CNBC's 'Closing Bell Overtime' with Kelly Evans and Jon Fortt, offered a sharp analysis of Microsoft's Q1 results, highlighting how the tech giant is not merely investing in AI but actively converting it into tangible financial gains, defying expectations of margin erosion.

Thill’s commentary began by addressing the market's initial reaction to Microsoft's Azure cloud growth, which, at 40% year-over-year, was a slight miss against street estimates of 38.2%. However, this narrow focus overlooks deeper indicators of commercial momentum. He emphasized that the street is "not picking up on the booking and the actual RPO," referring to Microsoft's commercial booking number at a robust 112% and its Remaining Performance Obligation (RPO) growing over 50%. These figures represent future revenue commitments, signaling an exceptionally strong demand pipeline.