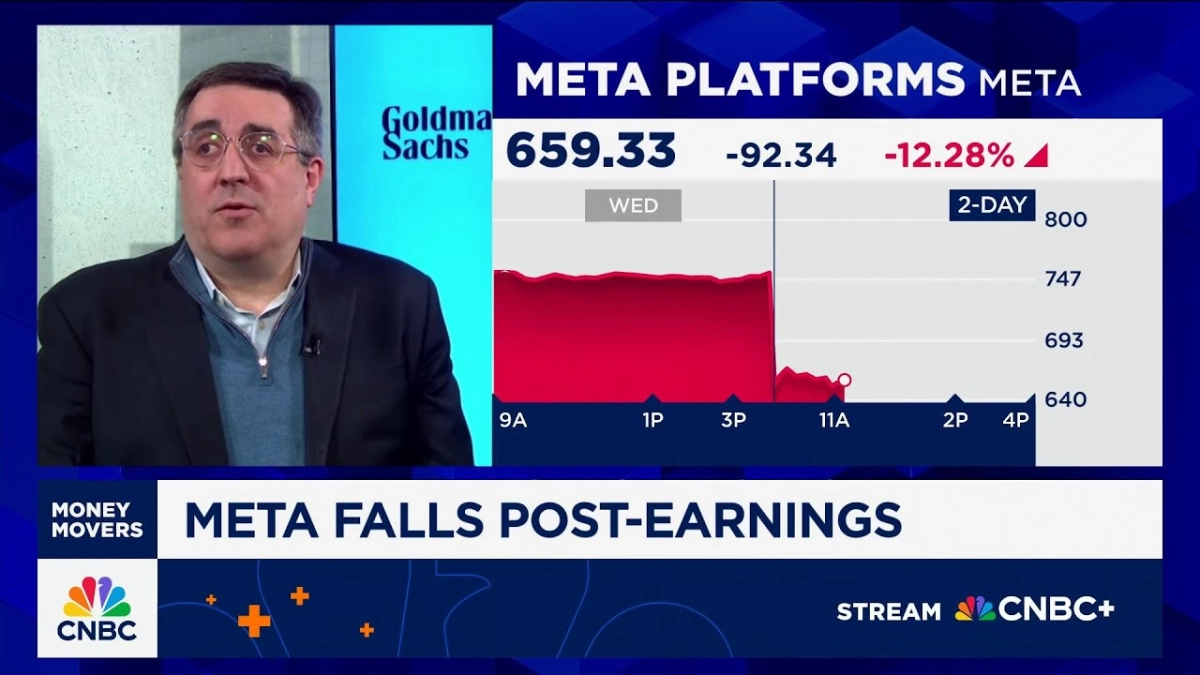

The market's patience for capital expenditure, particularly in the burgeoning field of artificial intelligence, has become a defining factor in big tech's recent earnings reactions. This sentiment was acutely underscored when Eric Sheridan, Goldman Sachs' Co-Head of Tech, Media, and Telecom Research, joined CNBC's "Squawk on the Street" team to dissect the third-quarter earnings of Alphabet and Meta. His analysis highlighted a stark divergence in investor confidence, largely driven by the immediate visibility of returns on significant AI and infrastructure investments.

Sheridan observed that the market currently places "a premium on visibility into return on capital spent," a standard Meta Platforms, despite its aggressive AI push, struggled to meet in the eyes of investors. Meta's stock experienced a sharp downturn of over 12% post-earnings, a reaction largely attributed to its substantial capital expenditure guidance for AI and Reality Labs, without a clear, near-term revenue correlative. This marks a critical juncture for companies pouring billions into foundational AI models and infrastructure, as the path to monetization remains an open question for many.