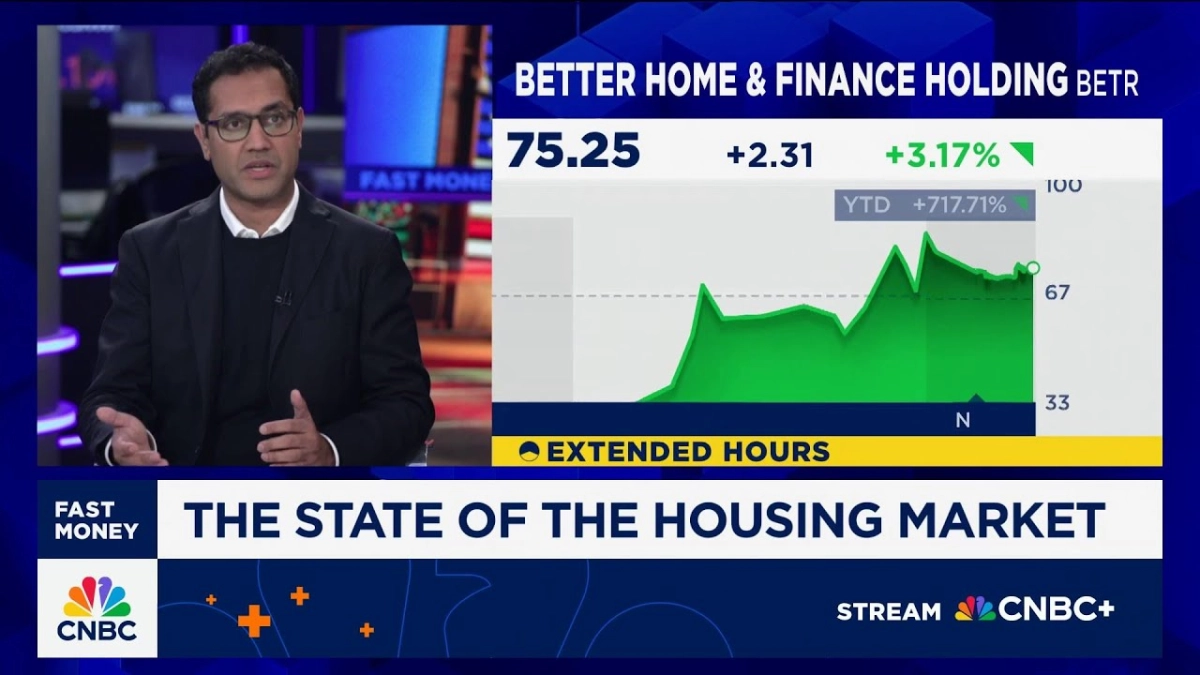

“Real AI is when you can take massive amounts of cost out of the system and deliver that back in savings to the consumer.” This assertion by Vishal Garg, Founder and CEO of Better.com, cuts through the current hype surrounding artificial intelligence, laying bare the true promise of the technology for established, often inefficient, industries. His recent appearance on CNBC’s Fast Money, alongside panelists Melissa Lee, Karen Finerman, Guy Adami, Dan Nathan, and Tim Seymour, offered a candid look into how Better.com is leveraging AI to disrupt the housing market and mortgage lending, particularly in the realm of refinancing and home equity.

The core of Better.com’s strategy, as articulated by Garg, is a profound commitment to cost reduction through technological innovation. He highlighted a significant market opportunity: an estimated 20 million Americans hold mortgages with rates exceeding 7%, acquired over the past three years. With Better.com offering rates around 6.2%, the potential for refinancing savings is substantial. For a $400,000 loan, this translates to roughly $3,200 in interest savings annually, a compelling proposition in an inflationary environment. This efficiency is not merely incremental; it's foundational to Better.com’s operational model.