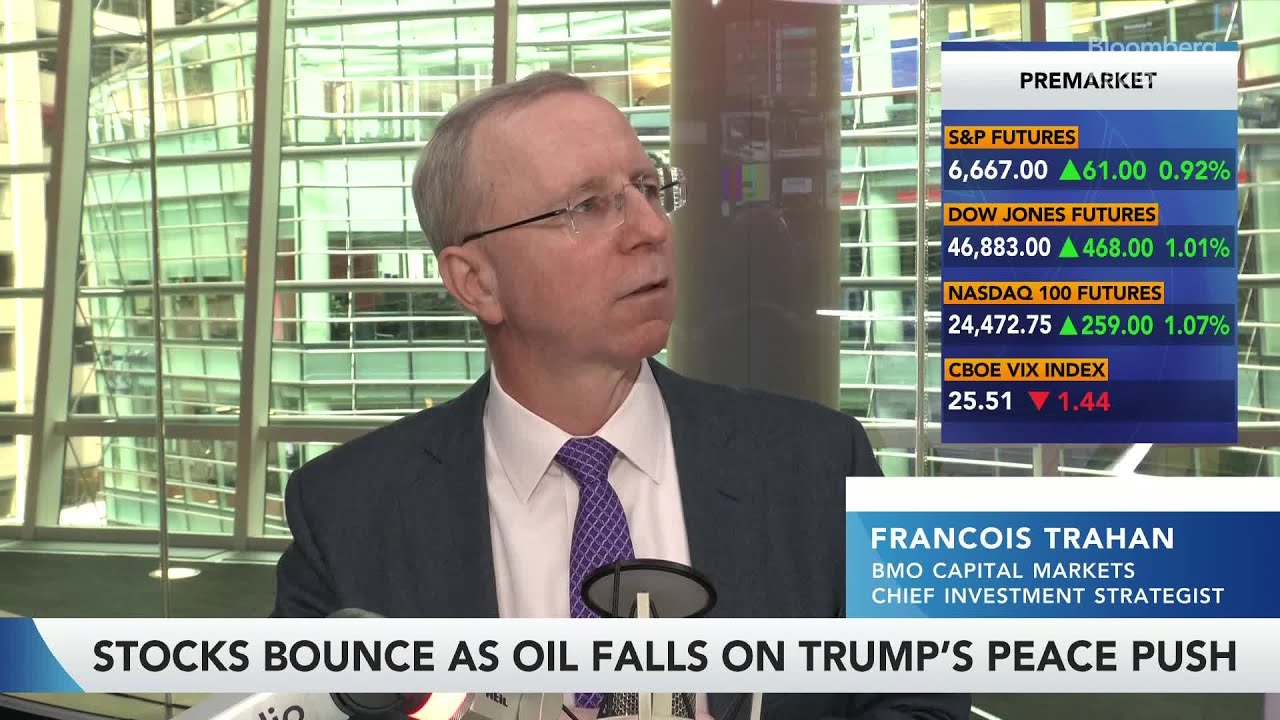

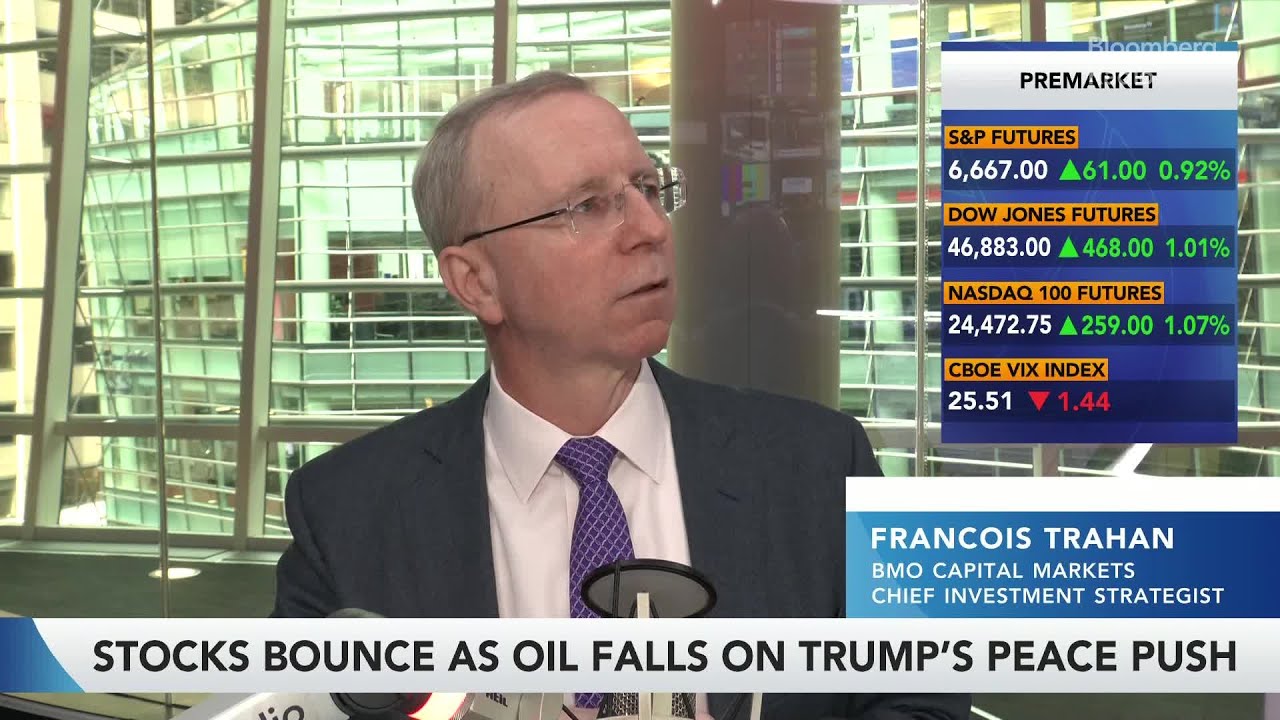

Francois Tirahon, Chief Investment Strategist at BMO Capital Markets, shared his economic outlook, suggesting that the US economy could face significant "friction" in 2025. Speaking on Bloomberg Radio, Tirahon highlighted that the current market sentiment is leaning towards a "soft landing," implying a controlled slowdown rather than a sharp recession. However, he cautioned that several factors could disrupt this optimistic scenario.

Francois Tirahon's Economic Outlook

Tirahon, a seasoned strategist with extensive experience in capital markets, pointed to a confluence of factors that could lead to a more challenging economic environment. He noted that the US economy has benefited from substantial stimulus measures and a period of low interest rates. However, as the Federal Reserve pivots towards tighter monetary policy to combat inflation, the availability of credit is expected to decrease, potentially impacting economic growth.