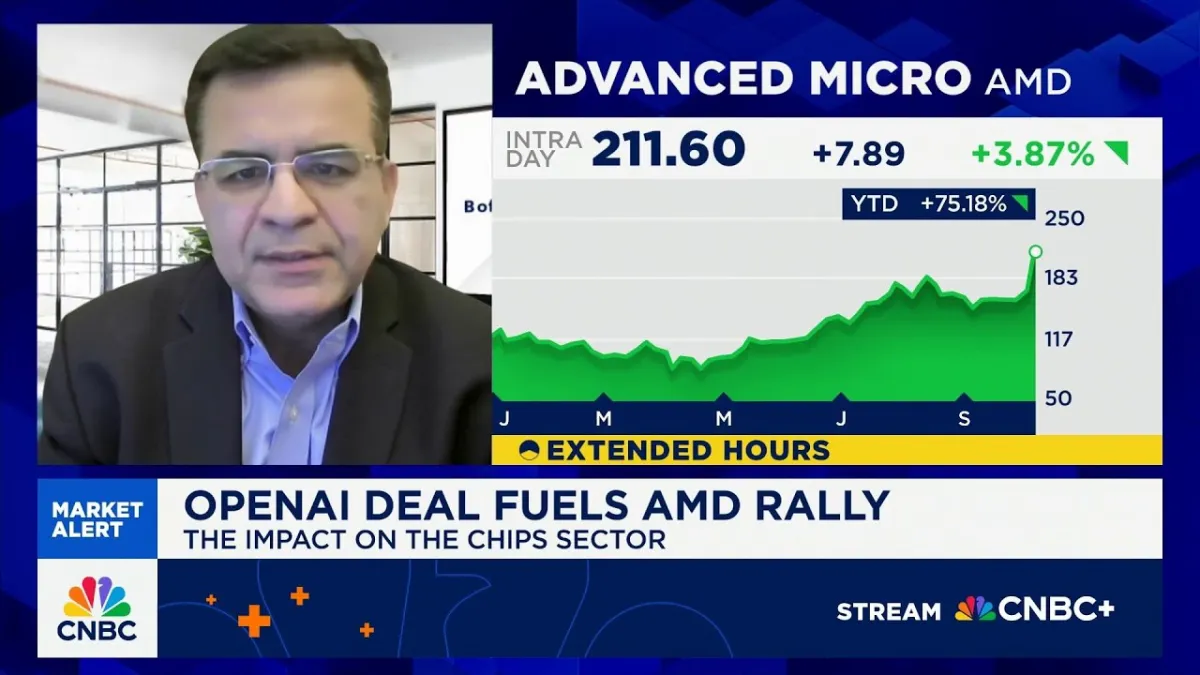

OpenAI is "eating computing power like Pac-Man," a vivid analogy offered by Vivek Arya, Senior Semiconductor Analyst at Bank of America Securities, during a recent interview on CNBC’s ‘Squawk Box.’ Arya's commentary underscored the insatiable demand for computational resources driven by generative artificial intelligence, a demand so profound that it is reshaping the semiconductor industry and inspiring a revised, bullish outlook for key players like Advanced Micro Devices (AMD). He spoke with the CNBC host about why Bank of America raised its price target on AMD to $250, up from $200, highlighting the profound implications of OpenAI's rapid expansion and its ripple effects across the chip sector.

Arya emphasized the sheer velocity of OpenAI’s user acquisition, noting their ascent to 800 million weekly active users, with projections to reach a billion by year-end. This remarkable growth occurred within three years of the company's formation, a stark contrast to the eight years it took Facebook to achieve the same milestone. Each of these users, Arya pointed out, is "consuming tremendous amount of tokens and computing capacity," creating an unprecedented need for robust infrastructure. This exponential consumption mandates a massive build-out of data center capabilities, a task OpenAI is undertaking with the assistance of cloud service providers and, crucially, leading semiconductor companies.